Flash Note

3 min

Mining for growth: navigating the small cap resource sector

Given our investment philosophy is ‘earnings drive share prices’, throughout the course of 2023 we have had – and benefited from – an overweight position in the Information Technology (IT) sector, based on company earnings expectations. Despite recent market volatility and shifting interest rate expectations, the sector has delivered a positive, fundamental change over the last two years with the shift from ‘growth at all costs’ to profitability and pursuing at-scale margin metrics.

Our view is the market will continue to look beyond the volatile and uncertain macro-economic landscape and focus on companies with sustainable earnings and long-term structural stories, which we are currently finding an abundance of in the IT sector as these companies gain exposure to structural themes of business digitisation, cloud computing and AI. While valuation multiples have re-rated for many stocks in the sector, our investment philosophy is based on the premise that valuation multiples can be supported provided earnings growth continues to surprise to the upside.

As interest rates increased over 2022-23, technology companies found it increasingly difficult to identify sustainable funding sources for their loss-making ‘growth at all costs’ business strategies. Many of these businesses have adapted to the changing market environment with most Australian small cap technology companies now reporting profitability over 2023, or intend on reaching that status over 2024-25.

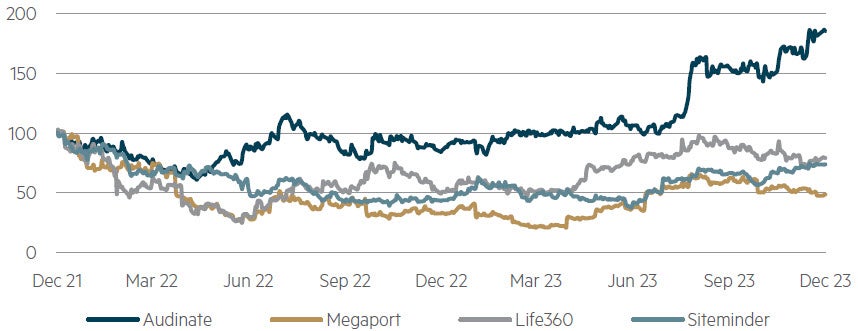

Below is a sub-set of Australian small cap technology stocks that incurred a significant sell-off in early 2022, with some share prices troughing in mid 2022, leading to a change in business strategy to accommodate the market’s desire for profitable and sustainable earnings streams.

Australian small cap tech – why we remain optimistic

Source: FactSet, MBA, share prices to 31 December 2023. Share prices indexed to 100 at starting date

These technology stocks saw their share prices recover over 2022-23 with the period between the troughs witnessed around July 2022 through to December 2023 seeing share prices multiply by an average of 2.5x, itemised separately:

Where we see earnings growth from the sector stems from structural trends which include:

More specifically, some of the quality Australian small cap technology company calls over the year highlight these key trends within their own businesses:

Data#3 (DTL): “We continue to drive transformation for our customers. And we are seeing rapid product development incorporating multi-cloud solutions with plenty of upside around services as we provide customers with more work in the cloud.” DTL, FY23 earnings transcript, 22 August 2023.

Megaport (MP1): “We're talking about huge amounts of data that need to then be dynamically moved around and it would depend on where you're going to train that model. So this is part of us delivering upon this AI explosion, but it doesn't rely upon the companies taking on AI. We've already got so many companies requesting for 100 gig connectivity where it makes sense. Now, this is exciting. This is a big deal for us.” MP1, Q1 sales and revenue call, 26 October 2023.

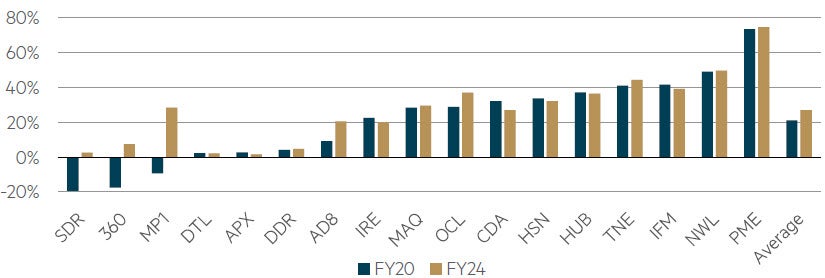

As the high-growth loss-making mentality in Australian small cap technology stocks has shifted to be more balanced between growth and profitability, companies in the space have restructured their cost bases (largely relating to employee expenses amid sticky wage inflation) and driven productivity enhancements from internal resource reallocation away from research & development to sales. These measures have created leaner organisations and has seen operating profit margins improve significantly.

The following chart contrasts the operating profit margin for select Australian small cap technology companies between the 2020 period of ultra-cheap financing to the 2024 period of ‘higher-for-longer’ interest rates. We observe that 12 out of the 17 companies in this cohort saw margins improve over this period.

EBITDA margins of Australian small cap tech companies – 2024 estimates vs 2020

Source: FactSet, MBA estimates, December 2023

As part of our ‘earnings drives share prices’ philosophy, we seek to identify companies with solid medium-term earnings prospects tied to a clear structural thematic. We believe Pro Medicus (PME), a world-class radiology imaging software business, is one such example. With a long history of meeting management, coupled with several industry expert meetings over the year, it’s evident to us that PME is experiencing an acceleration in contract award momentum in single academic and large hospital networks across the US, driving 30-40% per annum earnings growth on our estimate over the next few years.

We believe the company’s share price appreciation from $55 to $96 per share (+75%) over the 2023 calendar year has been driven by:

The recent Baylor Scott & White Health contract announcement represents a pivotal point in PME’s history with the contract value signed at $140m over the next ten years (vs historical contract values at ~$20m over 5-7 year periods). Our industry feedback from radiologists indicates that while PME has penetrated the most prestigious US hospital institutions, the business has merely scratched the surface in terms of radiology volumes in the US’s integrated delivery network (IDN) of hospitals. One of PME’s competitors, Sectra, was recently awarded a contract with a large US institution for $227m over the next ten years, painting a picture of what the path of accelerating contract win values may look like for PME from here.

PME’s entrance into cardiology and AI represents a significant opportunity to meet the market’s future demand (expanding PME’s addressable market by 40%) while providing incremental earnings at more attractive margins than what is currently produced (~74% EBITDA margins). While we are in the early stages of seeing these features launched, we believe once the US reimburses the use of AI algorithms in radiology exams the ramp up for PME’s AI Accelerator will be quicker than what the market expects.

Our investment thesis for PME continues to be based on increased earnings certainty and growth irrespective of the direction of bond yields – one of a number of exciting medium-term investment opportunities we believe are found within the Australian small cap technology sector.

The small cap technology sector has more recently been driven by the marked improvement in sector fundamentals, including the improved prospects for medium-term earnings growth, which we believe will continue for the sector – yet we appreciate that this is more pronounced in some companies than others. While there are always risks associated with investing in small cap companies, we believe the evolution of the technology sector to deliver more reliable quality earnings will continue to offer up exciting share price growth opportunities.

Disclaimer

This information was prepared and issued by Maple-Brown Abbott Ltd ABN 73 001 208 564, Australian Financial Service Licence No. 237296 (“MBA”). MBA is the Responsible Entity for the Maple-Brown Abbott Australian Small Companies Fund ARSN 658 552 688 (“the Fund”) This information must not be reproduced or transmitted in any form without the prior written consent of MBA. This information does not constitute investment advice or an investment recommendation of any kind and should not be relied upon as such. This information is general information only and it does not have regard to any person’s investment objectives, financial situation or needs. Before making any investment decision, you should seek independent investment, legal, tax, accounting or other professional advice as appropriate, and obtain the relevant Product Disclosure Statement and Target Market Determination for any financial product you are considering. This information does not constitute an offer or solicitation by anyone in any jurisdiction. This information is not an advertisement and is not directed at any person in any jurisdiction where the publication or availability of the information is prohibited or restricted by law. Past performance is not a reliable indicator of future performance. Any comments about investments are not a recommendation to buy, sell or hold. Any views expressed on individual stocks or other investments, or any forecasts or estimates, are point in time views and may be based on certain assumptions and qualifications not set out in part or in full in this information. The views and opinions contained herein are those of the authors as at the date of publication and are subject to change due to market and other conditions. Such views and opinions may not necessarily represent those expressed or reflected in other MBA communications, strategies or funds. Information derived from sources is believed to be accurate, however such information has not been independently verified and may be subject to assumptions and qualifications compiled by the relevant source and this information does not purport to provide a complete description of all or any such assumptions and qualifications. To the extent permitted by law, neither MBA, nor any of its related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained herein, or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this information. Neither MBA, nor any of its related parties, directors or employees, make any representation or give any guarantee as to the return of capital, performance, any specific rate of return, or the taxation consequences of, any investment. This information is current at 31 January 2024 and is subject to change at any time without notice. You can access MBA’s Financial Services Guide here for further information about any financial services or products which MBA may provide. © 2024 Maple-Brown Abbott Limited.

Interested in investing with us?

We believe it is through combining our earnings-based valuation approach with a focus on sustainability that the strategy will deliver enhanced investment performance in Australian small companies.